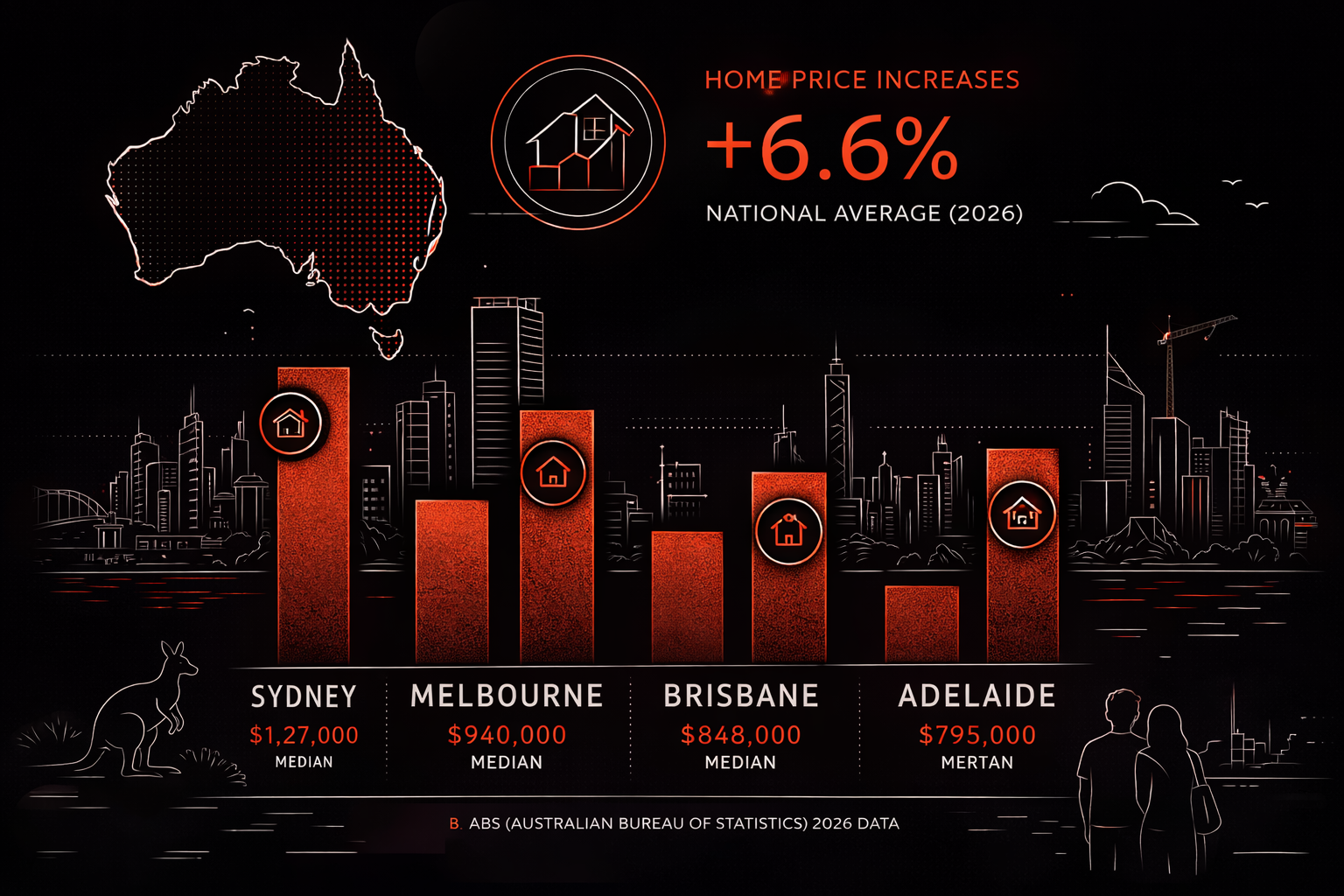

Home prices in Australia in 2026 remain among the highest relative to income of any country in the developed world, with Sydney’s median dwelling value sitting above $1.1 million and every major capital city recording prices that have, in real terms, outpaced wages by a significant margin over the past decade. The ABS Residential Property Price Indexes (RPPI) tell a story of a market shaped by structural undersupply, sustained population growth, and a rate cycle that pushed prices down briefly before they rebounded.

What the ABS Residential Property Price Indexes Measure

Before reading any headline figure, it helps to understand what the ABS is actually counting.

The ABS publishes its Residential Property Price Indexes quarterly, covering the eight state and territory capital cities. The index tracks the change in the price of established residential dwellings — it is a measure of movement, not a simple list of median sale prices. The ABS also publishes median price estimates alongside the index, which give a more tangible dollar figure for comparison.

A few things the RPPI does not capture:

- Price movements in regional areas outside the eight capitals

- New dwelling prices (tracked separately through other ABS series)

- Rental yields or investment returns

- Differences between houses and units within a city (though ABS does publish stratified data for some series)

This matters because national headlines often flatten significant variation — both between cities and within them.

City-by-City Home Price Breakdown

The table below draws on ABS RPPI median price estimates for established dwellings. Figures represent approximate medians for all dwelling types combined, based on the most recent available ABS data. Individual city trajectories are discussed in more detail below.

| Capital City | Approx. Median Dwelling Price | Est. Annual Change (YoY) | Median House Price | Median Unit Price |

|---|---|---|---|---|

| Sydney | ~$1,180,000 | +4.2% | ~$1,560,000 | ~$870,000 |

| Melbourne | ~$790,000 | +1.8% | ~$960,000 | ~$600,000 |

| Brisbane | ~$880,000 | +6.1% | ~$1,020,000 | ~$640,000 |

| Perth | ~$810,000 | +9.3% | ~$920,000 | ~$570,000 |

| Adelaide | ~$780,000 | +8.7% | ~$870,000 | ~$530,000 |

| Hobart | ~$560,000 | +1.2% | ~$620,000 | ~$480,000 |

| Darwin | ~$500,000 | +2.4% | ~$560,000 | ~$400,000 |

| Canberra | ~$840,000 | +2.9% | ~$990,000 | ~$610,000 |

Source: ABS Residential Property Price Indexes, most recent available quarterly release. Figures are indicative approximations and should not be used for financial decision-making. Annual change estimates are directional and based on available ABS data at time of publication.

Sydney

Sydney remains Australia’s most expensive property market by a wide margin. The gap between the median house price and the median unit price — roughly $690,000 — is itself larger than the total median dwelling price in Darwin or Hobart. Affordability constraints have increasingly pushed first home buyer activity toward units and outer-ring suburbs, where prices are somewhat lower but still represent a substantial financial commitment.

Melbourne

Melbourne is the outlier among the larger capitals. Price growth has been noticeably softer than Brisbane, Perth, and Adelaide, in part due to higher land tax rates introduced by the Victorian state government, a higher rate of new dwelling completions relative to other cities, and a somewhat slower recovery in population growth post-pandemic. Melbourne’s relative softness has attracted commentary from analysts watching for signs of a broader market correction — but the data shows modest growth, not decline.

Brisbane and South-East Queensland

Brisbane has seen consistent price growth since 2021, driven initially by interstate migration from NSW and Victoria, and more recently by infrastructure spending associated with the 2032 Olympic Games. The unit market in Brisbane has strengthened considerably as buyers priced out of houses have shifted demand down the property type ladder.

Perth and Adelaide

Perth and Adelaide have been the standout performers nationally over the past two years. Both cities entered the current price cycle with significantly lower median prices than Sydney and Melbourne, attracting both owner-occupiers and investors who perceived relative value. In Perth’s case, the strength of the resources sector and a tight labour market have supported local incomes and buyer demand. In Adelaide, a constrained land release pipeline has been a key factor.

The pace of growth in both cities has prompted questions about sustainability. A market growing at 8–9% annually, against a backdrop of flat or modestly rising incomes, is by definition compressing affordability — even if absolute prices remain lower than the east coast.

Hobart and Darwin

Both cities experienced sharp price run-ups during 2020–2022 and have since moderated significantly. Hobart in particular saw unusually strong growth driven by lifestyle migration during COVID lockdowns, which pulled forward demand that the market has since digested. Both remain more accessible in absolute price terms than any mainland capital.

What Is Driving Australian Home Prices in 2026?

Population Growth and Migration

Australia’s population grew at an elevated pace through 2022 and 2023. ABS data recorded net overseas migration of approximately 518,000 in the year to June 2023 before moderating. That population base needs to be housed — and a material share of new arrivals eventually move from renting to purchasing. The demographic pipeline of demand does not switch off quickly even as migration numbers normalise.

Domestically, internal migration patterns have shifted. The share of Australians moving from Sydney and Melbourne toward Brisbane, Perth, and Adelaide accelerated post-pandemic and has not fully reversed. This has contributed directly to price divergence between the cities recording the fastest growth and those that have moderated.

Supply Shortfall

The single most persistent structural driver of Australian home prices is the gap between housing demand and housing supply. The National Housing Accord’s target of 1.2 million new homes over five years requires approximately 240,000 completions per year. ABS building approvals data shows completions have consistently tracked around 160,000 per year — a shortfall of roughly 33% against target.

Construction cost inflation, trade labour shortages, planning delays, and rising land prices have all constrained the pipeline. The result is that even as demand has normalised from its post-pandemic peak, supply has not caught up, keeping price floors elevated.

The Interest Rate Cycle

The RBA’s rate hiking cycle — 13 increases between May 2022 and November 2023, taking the cash rate from 0.10% to 4.35% — caused a meaningful price correction in 2022 and into early 2023, with national dwelling values falling approximately 8–9% from their peak. The correction was uneven: Sydney and Melbourne fell further, while Brisbane, Perth, and Adelaide barely paused.

From late 2023 and through 2024, prices resumed their upward trajectory as the market absorbed the rate environment and expectations of eventual cuts took hold. For context on how the RBA’s 2026 rate decisions are affecting the property market, see our full RBA interest rate timeline for 2026.

The key dynamic: when rates were low, prices rose because borrowing was cheap. When rates rose, prices fell only partially and briefly — because the supply constraint placed a floor under values that monetary policy alone could not remove.

The Affordability Problem in Numbers

Price-to-income ratios are a standard measure of housing affordability. A ratio of 3–4 times median household income is considered moderately affordable. Australia’s major cities have moved well beyond that range.

Using ABS median full-time adult earnings of approximately $98,800 per year, and the median dwelling prices above:

- Sydney price-to-income ratio: approximately 11.9x

- Perth: approximately 8.2x

- Adelaide: approximately 7.9x

- Melbourne: approximately 8.0x

- Brisbane: approximately 8.9x

On any international measure, ratios above 5x are classified as “severely unaffordable.” Every Australian capital city sits in that category. Sydney and Melbourne consistently rank among the top 10 least affordable cities globally in annual housing affordability surveys.

For households on lower incomes — including those on the minimum wage or receiving government payments — ownership in a capital city is, in practice, inaccessible without family equity transfer or exceptional saving capacity. For renters weighing up whether to continue renting or attempt to enter the market, our breakdown of the rental crisis data in 2026 provides the affordability context for the rental side of the ledger.

What First Home Buyers Are Actually Doing

ABS Housing Finance data tracks the number and value of loans to first home buyers each month. The data through 2024 shows that first home buyer activity:

- Has shifted heavily toward apartments and townhouses rather than detached houses in Sydney and Melbourne

- Is increasingly concentrated in outer metropolitan growth corridors where land release has added supply

- Has been partially supported by federal and state first home buyer schemes — including deposit guarantees, stamp duty concessions, and shared equity programmes

Take-up of government first home buyer schemes has been significant, though capacity caps on some programmes mean not every eligible applicant can access them. Our complete guide to First Home Buyer schemes in 2026 covers current eligibility thresholds, what each scheme actually provides, and the data on how many buyers have used them.

Houses vs Units: A Diverging Market

One structural shift in the 2025–26 price data is the narrowing, in some cities, of the gap between house and unit prices. As house prices have become increasingly inaccessible, demand has flowed into units — driving unit price growth in some markets to outpace house price growth for the first time in years.

This is particularly visible in:

- Brisbane, where the unit market lagged for years due to oversupply from a prior construction boom and has now absorbed that excess

- Perth, where investor demand has been strong across both property types

- Sydney, where the house-unit price gap is so large that units in middle-ring suburbs represent the only accessible entry point for many buyers

The relative outperformance of units in these markets has implications for investors. Capital gains tax treatment applies to both property types — our capital gains tax guide for property owners in 2026 covers the ATO rules on how gains are calculated and what the 50% discount means for properties held longer than 12 months.

FAQ

What is the average home price in Australia in 2026?

Based on the most recent available ABS Residential Property Price Indexes data, the national weighted average median dwelling price across the eight capital cities sits approximately in the $840,000–$900,000 range. This varies significantly by city — Sydney’s median is above $1.1 million while Darwin’s sits around $500,000.

Which Australian city has the cheapest home prices in 2026?

Darwin has the lowest median dwelling price among the eight capital cities, followed by Hobart. Both cities have more modest local economies and smaller populations than the mainland capitals, which keeps absolute prices lower — though price-to-income ratios are still above what would be considered affordable by international standards.

Are Australian home prices going to fall in 2026?

The ABS RPPI data does not support predictions — it measures what has happened, not what will. As of the most recent available data, prices are growing in most capitals, with Perth and Adelaide leading. A material correction would likely require a significant demand shock — such as a sharp rise in unemployment or a further rate increase cycle — or a sudden acceleration in housing supply. The current data does not signal either as imminent.

Why are Perth and Adelaide growing faster than Sydney and Melbourne?

Both cities entered the current cycle at lower absolute price levels, attracting buyers who perceived relative value. Perth benefits from a strong resources sector supporting local incomes and employment. Adelaide has a constrained land pipeline and has experienced sustained interstate migration. Sydney and Melbourne are growing more slowly from a much higher base, with affordability constraints limiting the pool of potential buyers.

How does the ABS measure property prices?

The ABS Residential Property Price Indexes track price change in established residential dwellings across the eight capital cities using a hedonic regression methodology that controls for changes in the mix of properties sold. The indexes are published quarterly, along with stratified median price data. The full methodology is available at the ABS Residential Property Price Indexes page.

Conclusion

Australian home prices in 2026 reflect a market shaped by decades of undersupply, sustained population growth, and an interest rate cycle that corrected values only partially before they resumed climbing. The city-by-city ABS data shows a two-speed market: Perth and Adelaide growing rapidly from a lower base, Sydney and Melbourne grinding higher from already unaffordable levels, and Melbourne softening relative to its peers. For buyers, renters, and investors, the structural picture has not changed materially — supply is too low, demand remains elevated, and affordability ratios are, in most cities, at or near historically severe levels.

This article is for informational purposes only and does not constitute financial, legal, or investment advice. Data is sourced from publicly available Australian government sources and is accurate at time of publication. Property markets are subject to rapid change. Please consult a registered professional for advice specific to your situation.