Rent vs buy in Australia in 2026 is the most consequential financial question millions of Australians face — and the honest answer is more complicated than either camp wants to admit. Renting is cheaper month-to-month in every major city. Buying builds long-term wealth that renting never can. The right answer depends entirely on your city, your timeline, your deposit, and what you do with the money you save by renting.

Here is what the data actually shows.

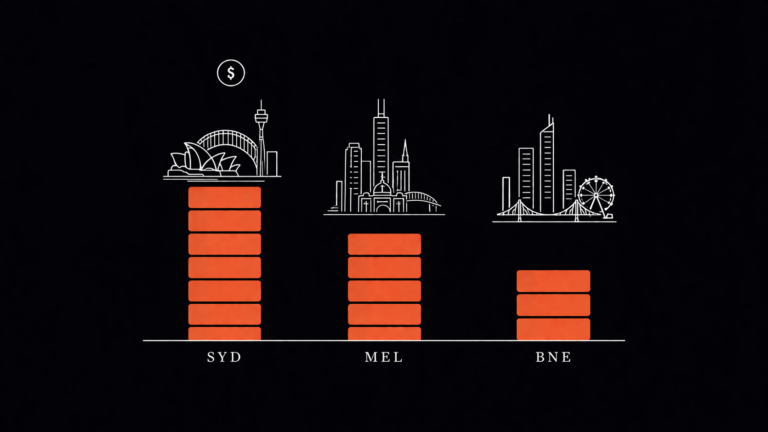

The Monthly Cost Gap — Buying Costs More Everywhere Right Now

In every major Australian city in 2026, monthly mortgage repayments exceed the equivalent cost of renting. The gap is largest in Sydney, according to Finder’s December 2025 research:

| City | Average monthly mortgage | Average monthly rent |

|---|---|---|

| Sydney | $7,275 | $3,211 |

| Melbourne | Higher than rent | Lower than mortgage |

| Brisbane | Higher than rent | Lower than mortgage |

| Adelaide | Higher than rent | Lower than mortgage |

| Perth | Higher than rent | Lower than mortgage |

Sydney’s gap is the most extreme — mortgage repayments are more than double the cost of renting. On an annual basis, a Sydney buyer with an 80 per cent LVR loan on the median $1.75 million house pays approximately $105,000 in interest alone in the first year — before maintenance, council rates, insurance, and strata. The equivalent annual rent for that same property is approximately $39,000.

That is an extra $66,000 per year in costs — just in interest — before you count a cent of principal repayment.

But Renting Is Not Free Either

The counter-argument is not that renting is cheap — it is that renting is less expensive right now than the alternative.

Australia’s rental market is under severe stress. The national median rent reached $650 per week in mid-2025, up 44 per cent over five years. 46 per cent of Australian renters are currently struggling to afford their rent, according to Finder’s December 2025 survey.

The states hardest hit by rental stress are Tasmania at 78 per cent of renters struggling and Victoria at 64 per cent. Even the ACT — the lowest — recorded 29 per cent of renters under pressure.

Renting is cheaper in dollar terms right now. But renting in a market with a 1.2 per cent vacancy rate carries its own risks — landlords selling, rent increases, forced moves, and zero security of tenure. For the full picture of what is driving rents, see our rent prices guide.

The Long-Term Wealth Argument for Buying

The case for buying is not about monthly cash flow — it is about what happens over 20 to 30 years.

Australian property prices have grown at an average of 5.4 per cent per year historically. On a $1 million property purchased today, that growth compounds to a significantly larger asset over three decades. A buyer who purchases that property and holds it for 30 years ends with an asset worth approximately $3.25 million — despite paying approximately $2 million in total mortgage costs over that period.

The renter who pays the equivalent in rent over 30 years — at 3.8 per cent yield, approximately $38,000 annually — pays out $1.14 million in rent and owns nothing at the end.

That is the core long-term wealth argument for buying — and it is a compelling one. The question is whether the short-term cost difference is manageable enough to get there.

The Deposit Problem

The biggest barrier to buying in 2026 is not the mortgage repayment — it is accumulating the deposit.

On a Sydney median house of $1.75 million, a 20 per cent deposit is $350,000. Add stamp duty and transaction costs of approximately 5 to 6 per cent of the purchase price and the total upfront cash required before you make a single repayment is approximately $450,000 to $460,000.

Even with the federal government’s Home Guarantee Scheme — which allows eligible first home buyers to purchase with as little as 5 per cent deposit without paying Lenders Mortgage Insurance — the minimum deposit on a Sydney median house is still $87,500.

The opportunity cost of that deposit is real. In early 2026, high interest savings accounts are paying 4.5 to 5.5 per cent. A $350,000 deposit sitting in a HISA earns approximately $17,500 per year in interest — money the buyer effectively gives up when they tie that capital into a property. This does not make buying wrong — but it must be factored into any honest comparison.

The Break-Even Point — When Buying Wins

Buying almost never makes financial sense in a short time horizon. Transaction costs alone — stamp duty, legal fees, inspection costs — typically equal 5 to 6 per cent of the purchase price. On a $1 million property, that is $50,000 to $60,000 in costs you pay before the property increases in value at all.

Based on current data and bank forecasts:

- CBA and Westpac forecast Sydney property growth of 4 to 5 per cent for 2026

- The break-even point — when buying produces better net wealth than renting and investing the difference — is typically 5 to 10 years in most Australian markets

- In Melbourne, where prices have been soft since 2022 and rental yields have risen sharply, the break-even is longer — renting and investing the deposit in a HISA often produces a better 1 to 3 year outcome

The implication: if you plan to stay in a property for fewer than 5 years, renting and investing the deposit difference is almost always the better financial outcome. If you plan to stay for 10 or more years, buying almost always wins through capital growth and equity.

Rentvesting — The Third Option

An increasing number of Australians are rejecting the binary rent-or-buy choice entirely. 54 per cent of Australian first home buyers are now considering rentvesting — renting where they want to live and buying an investment property in a more affordable market. That figure is up from 50 per cent in 2024.

Rentvesting allows buyers to enter the property market at a lower price point, access tax deductions on investment loan interest, and maintain the lifestyle flexibility of renting in their preferred suburb. The trade-off is the complexity of managing a tenancy, the emotional disconnect of not owning your own home, and the capital gains tax implications when selling.

Key Takeaways — Rent vs Buy Australia 2026

Buying costs significantly more than renting in every major Australian city right now. Sydney’s monthly mortgage gap is the widest — $7,275 to buy versus $3,211 to rent. But renting builds no equity, provides no security, and exposes you to ongoing market rent increases in a market with historically low vacancy.

The honest answer: renting is the better short-term cash flow decision. Buying is the better long-term wealth building decision — if you can sustain the higher monthly costs, have a genuine deposit, and plan to hold for at least 5 to 7 years.

For context on what is driving the housing market, see our house prices guide, our mortgage stress article, and our Sydney vs Melbourne vs Brisbane comparison — Sydney vs Melbourne vs Brisbane Cost of Living 2026 — Which City Is Actually Cheaper?

This article is for general informational purposes only and reflects the author’s own research and understanding of publicly available data. Property prices, mortgage rates, and rental yields change regularly. Always seek independent financial and legal advice before making property decisions.